MyLife Checking

- No monthly maintenance fees

- No minimum balance requirements

- Get paid up to 2 days early with direct deposit1

MyLife Checking is the go-to account for your everyday needs.

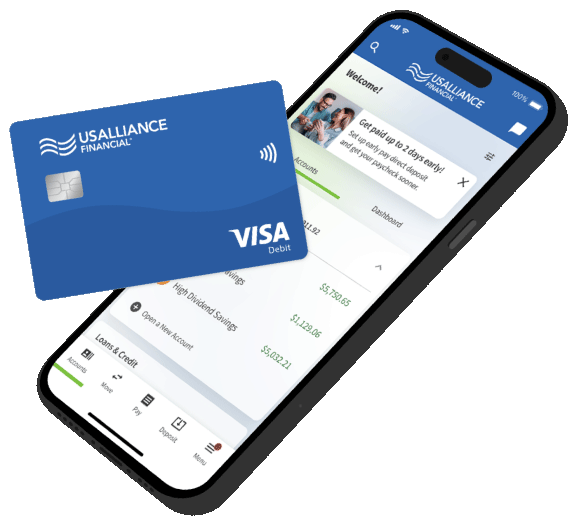

Your checking account should adapt to you, not the other way around. That’s why with MyLife Checking you can use your Visa® debit card at checkout, pair it with your mobile wallet for contactless payments, and keep track of your finances on the go with USALLIANCE’s digital banking app. However you bank or shop, you can rely on MyLife Checking.

No Maintenance Fees or Minimum Balance Requirements

MyLife Checking is a free, no-hassle checking account, so there are no monthly maintenance fees or minimum balances to worry about.

Get Paid Early with Direct Deposit

When you set up direct deposit, you can get access to your paycheck up to two days early!1

Access 33,000+ No-Fee ATMs, Get Refunded for Outside ATMs

You’ll have access to over 33,000 surcharge-free ATMs, but we’ll also refund you the same day for non-USALLIANCE ATM fees, up to $25 per month.2

Add Cash

Deposit cash into your account at thousands of retail locations nationwide, giving you a convenient way to manage your money while you’re already out and about!4

Additional Features

Free Credit Score Monitoring

Keep an eye on your finances with free credit score monitoring – delivered directly to your digital banking dashboard each month.

Overdraft Protection and Privilege

You won't be charged overdraft fees when a single transaction is under $5 or your account is overdrawn by $5 or less.3

VISA® Debit Card Alerts

Receive custom alerts about your debit card activity sent to you via text message. Update your preferences anytime with digital banking.

MyLife Checking is the go-to account for your everyday needs.

Your checking account should adapt to you, not the other way around. That’s why with MyLife Checking you can use your Visa® debit card at checkout, pair it with your mobile wallet for contactless payments, and keep track of your finances on the go with USALLIANCE’s digital banking app. However you bank or shop, you can rely on MyLife Checking.

No Maintenance Fees or Minimum Balance Requirements

MyLife Checking is a free, no-hassle checking account, so there are no monthly maintenance fees or minimum balances to worry about.

Get Paid Early with Direct Deposit

When you set up direct deposit, you can get access to your paycheck up to two days early!1

Access 33,000+ No-Fee ATMs, Get Refunded for Outside ATMs

You’ll have access to over 33,000 surcharge-free ATMs, but we’ll also refund you the same day for non-USALLIANCE ATM fees, up to $25 per month.2

Add Cash

Deposit cash into your account at thousands of retail locations nationwide, giving you a convenient way to manage your money while you’re already out and about!4

Additional Features

Free Credit Score Monitoring

Keep an eye on your finances with free credit score monitoring – delivered directly to your digital banking dashboard each month.

Overdraft Protection and Privilege

You won't be charged overdraft fees when a single transaction is under $5 or your account is overdrawn by $5 or less.3

VISA® Debit Card Alerts

Receive custom alerts about your debit card activity sent to you via text message. Update your preferences anytime with digital banking.

.webp?width=250&height=212&name=COOP-USALLIANCE-red%20(1).webp)